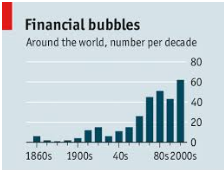

Yellen Says No More Financial Panics in Her Lifetime

Janet Yellen finally did it, mark the date June 27, 2017. Something all modern Federal Reserve chairs do: open mouth, insert foot. Today in London Ms. Yellen announced the end of financial panics...well...at least while she’s alive.

"Would I say there will never, ever be another financial crisis? You know probably that would be going too far but I do think we're much safer and I hope that it will not be in our lifetimes and I don't believe it will be," Yellen said.

She follows in the footsteps of two great Fed Chair prognosticators.

In 2002 Alan Greenspan said,

The ongoing strength in the housing market has raised concerns about the possible emergence of a bubble in home prices. However, the analogy often made to the building and bursting of a stock price bubble is imperfect. First, unlike in the stock market, sales in the real estate market incur substantial transactions costs and, when most homes are sold, the seller must physically move out. Doing so often entails significant financial and emotional costs and is an obvious impediment to stimulating a bubble through speculative trading in homes. us, while stock market turnover is more than percent annually, the turnover of home ownership is less than percent annually— scarcely tinder for speculative conflagration. Second, arbitrage opportunities are much more limited in housing markets than in securities markets. A home in Portland, Oregon is not a close substitute for a home in Portland, Maine, and the “national” housing market is better understood as a collection of small, local housing markets. Even if a bubble were to develop in a local market, it would not necessarily have implications for the nation as a whole.

When Federal Reserve Chairman Ben Bernanke was questioned in 2005 about whether house prices might be getting ahead of the fundamentals, he replied:

Well, I guess I don’t buy your premise. It’s a pretty unlikely possibility. We’ve never had a decline in house prices on a nationwide basis. So what I think is more likely is that house prices will slow, maybe stabilize: might slow consumption spending a bit. I don’t think it’s going to drive the economy too far from its full employment path, though.

Also in 2005.

House prices have risen by nearly 25 percent over the past two years. Although speculative activity has increased in some areas, at a national level these price increases largely reflect strong economic fundamentals.

Later that same year

With respect to their safety, derivatives, for the most part, are traded among very sophisticated financial institutions and individuals who have considerable incentive to understand them and to use them properly.

Then in 2006

Housing markets are cooling a bit. Our expectation is that the decline in activity or the slowing in activity will be moderate, that house prices will probably continue to rise.

February 2007

Despite the ongoing adjustments in the housing sector, overall economic prospects for households remain good. Household finances appear generally solid, and delinquency rates on most types of consumer loans and residential mortgages remain low.

March 2007

At this juncture, however, the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained. In particular, mortgages to prime borrowers and fixed-rate mortgages to all classes of borrowers continue to perform well, with low rates of delinquency.

May 2007

All that said, given the fundamental factors in place that should support the demand for housing, we believe the effect of the troubles in the subprime sector on the broader housing market will likely be limited, and we do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system. The vast majority of mortgages, including even subprime mortgages, continue to perform well. Past gains in house prices have left most homeowners with significant amounts of home equity, and growth in jobs and incomes should help keep the financial obligations of most households manageable.

October 2007

It is not the responsibility of the Federal Reserve – nor would it be appropriate – to protect lenders and investors from the consequences of their financial decisions.

June 2008

The risk that the economy has entered a substantial downturn appears to have diminished over the past month or so.

July 2008

The GSEs are adequately capitalized. They are in no danger of failing.

December 2010

I wish I'd been omniscient and seen the crisis coming.